Back

Insights

EU Economy: Weekly Commentary – November 03, 2025

European Market Review

Adrian Van Den Bok and David Pintado

CEO

European Market Review

European bond yields fell except in Germany; Italian debt attracted attention as Scope Ratings upgraded its outlook. Equities were mixed, euro weakened, and Brent crude declined amid supply and demand concerns.

European bond yields mostly declined last week, with the exception of Germany, where the 10-year yield rose slightly by 0.60 basis points. Italian debt remained in focus as Prime Minister Giorgia Meloni advanced efforts to restore the country’s credibility as a borrower, with Scope Ratings upgrading Italy’s outlook in recognition of improved fiscal prospects and confidence in ongoing reforms. Italian 10-year government bonds fell nearly 3 basis points amid volatility linked to investor reassessment of fiscal policies and broader European market trends, while the France-Italy 30-year spread fell to zero basis points for the first time since 1998. European equities closed the week with mixed results, as markets in Italy, Spain, and Portugal rose while other major indices retreated. The euro depreciated 0.77% against the US dollar. Brent crude declined 1.69% on expectations that the Federal Reserve may pause interest rate cuts, combined with rising global supply, geopolitical tensions in Venezuela, and weak Chinese economic data that weighed on demand forecasts. Initial optimism over US-China trade negotiations faded following OPEC+ indications of production increases and rising US output. A stronger dollar and slowing Chinese manufacturing activity added further downward pressure, with investor attention now focused on the next OPEC+ meeting, where additional output could further influence prices.

Week: 27 – 31 October | |||||

Stock Market | Last | % CHG | Currency | Last | % CHG |

Euro Stoxx | 5662.04 | -0.22 | EUR/USD | 1.1536 | -0.77 |

Stoxx Europe 600 | 571.89 | -0.67 | Commodities | Last | % CHG |

France | 8121.07 | -1.27 | Brent | 64.58 | -1.69 |

Germany | 23958.30 | -1.16 | Bond Market - 10 Years | Last | BP |

Italy | 43175.32 | 1.62 | Germany | 2.634% | 0.60 |

Portugal | 8426.96 | 0.69 | France | 3.422% | -1.61 |

Spain | 16032.60 | 1.08 | Italy | 3.363% | -2.81 |

Belgium | 4902.37 | -1.84 | Spain | 3.149% | -1.62 |

Europe View Synopsis

The ECB kept rates at 2%, citing stable inflation and growth. Eurozone GDP rose 0.2% in Q3. Inflation eased to 2.1%. Risks remain, no rate cuts expected.

At its October meeting in Florence, the European Central Bank (ECB) kept key interest rates at 2.00%, remaining in its ‘good place’ with stable inflation and growth forecasts, while providing no guidance on future rate paths. Eurozone GDP rose 0.2% QoQ in Q3, led by France at 0.5% and Spain at 0.6%, while Germany and Italy stagnated, reflecting uneven growth amid structural challenges, underinvestment, and geopolitical pressures. The ECB expects modest expansion of 0.8% in 2025 and 0.9% in 2026, with risks from US tariffs, a stronger euro, political uncertainty, and supply chain disruptions. Headline inflation eased slightly to 2.1% YoY in October due to lower energy prices, while core inflation remained elevated at 2.4%, driven by resilient services prices at 3.4% YoY. The ECB described the current inflation environment as stable, supporting its cautious, data-driven approach. If conditions remain steady, further rate cuts this year are unlikely, reflecting the Bank’s balance between measured optimism on growth and vigilance against emerging risks.

Interest Rate Decision

The ECB kept rates at 2.00%, remained in its ‘good place,’ noted stable inflation and growth forecasts, and gave no guidance on future rate paths.

The European Central Bank (ECB) maintained its key interest rates at the October meeting in Florence, keeping the deposit rate at 2.00% as widely expected and signalling no commitment to a predetermined path for future rate adjustments. Holding its only annual meeting outside Frankfurt, President Christine Lagarde described Florence as a ‘magnificent’ setting, while the Bank continued to operate from what it calls its ‘good place,’ comfortably maintaining rates. ECB growth forecasts project the Eurozone economy to expand slightly above 1% annually, with inflation gradually stabilizing near 2%, supporting the decision to maintain the current policy stance. Nonetheless, several downside risks could influence future policy, including delayed effects from US tariffs, a stronger euro, political uncertainty in France, slower-than-expected implementation of Germany’s fiscal stimulus, and potential supply chain disruptions linked to EU-China tensions in microchips and rare earths. The ECB also noted that the inflation outlook is broadly unchanged, with the 2027 forecast factoring in a 0.2 percentage-point impact from the ETS2 system, meaning any delay could raise the risk of undershooting its target, making 2028 projections particularly important. The meeting highlighted the ECB’s cautious, data-driven approach, balancing optimism on growth and inflation with vigilance against emerging risks, while clearly signalling its intention to remain in its ‘good place’ for the foreseeable future.

If conditions remain stable and no abrupt changes occur, we do not expect further rate cuts from the ECB this year.

GDP

Eurozone GDP rose 0.2% QoQ in Q3. France improved, while Germany and Italy stagnated and Spain’s expansion moderated; rising sentiment contrasts with ongoing political, fiscal, and global uncertainties.

Eurozone GDP grew by 0.2% QoQ in the third quarter, slightly above expectations, though it is too early to interpret this as the start of a sustained growth acceleration amid persistent domestic and global uncertainties. Performance varied across member states. France recorded a strong 0.5% QoQ increase, supported by robust investment, rising exports—particularly in the aerospace sector—and resilient domestic demand, with household consumption up 0.1% QoQ and government spending rising 0.5% QoQ, while inventory adjustments subtracted 0.6 percentage points from growth. Spain moderated to 0.6% QoQ from 0.8% QoQ but continued to outperform the Eurozone average, benefiting from stable domestic demand and solid exports. External trade provided a boost in several economies, and surveys of economic sentiment, including the PMI and European Economic Sentiment Indicator, rose in October to 96.7 from 95.6, reflecting cautious optimism among businesses and consumers despite elevated household savings and slowing global demand.

Germany and Italy remained flat at 0.0% QoQ, with Germany narrowly avoiding a technical recession after a revised -0.2% QoQ contraction in Q2. Germany’s stagnation underscores deep structural challenges, including underinvestment, rising production costs, labour shortages, and declining international competitiveness, compounded by geopolitical pressures such as Chinese export controls on microchips affecting the automotive sector. While the government has announced €500 billion in fiscal stimulus for infrastructure and defence, recent budget adjustments and political uncertainty are likely to delay its full impact, with much of the benefit expected only in 2027. Modest Q3 investment was offset by weak exports and subdued private consumption, highlighting the fragility of growth. Overall, the Eurozone economy has avoided recession, but broad-based acceleration remains limited, with GDP projected at 0.8% in 2025 and 0.9% in 2026, and ongoing fiscal, political, and structural risks continuing to shape the outlook.

We expect the Eurozone economy to continue showing limited improvement. Growth will be constrained by Germany and France, both of which are very weak economies.

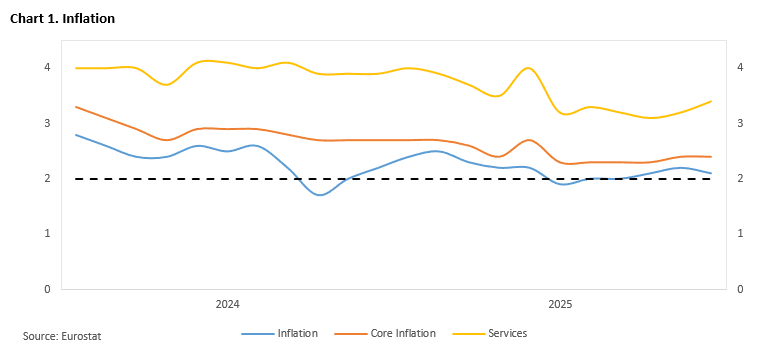

Inflation

Eurozone headline inflation eased to 2.1% YoY in October, driven by lower energy prices, while core inflation remained 2.4% YoY; services rose 3.4%, sustaining ECB’s cautious stance.

Eurozone headline inflation moderated slightly to 2.1% YoY in October, down from 2.2% YoY, driven primarily by easing energy price developments (-1.0% YoY), while core inflation remained elevated at 2.4% YoY, reflecting sustained strength in services prices. Services inflation accelerated further from 3.2% to 3.4% YoY, well above pre-pandemic levels, underscoring the ongoing resilience of the sector, whereas food, alcohol, and tobacco prices increased by 2.5% YoY and other goods by 0.6% YoY. The European Central Bank has described the current inflation environment as its ‘good place,’ with headline inflation remaining within 0.2 percentage points of the 2% target since March, providing support for its recent decision to maintain interest rates. Short-term dynamics indicate a modest acceleration in core inflation momentum, with the three-month annualized rate rising to 2.7% YoY, though easing services selling price expectations point to limited upside pressures ahead. ECB President Christine Lagarde has highlighted the persistent elevation of services inflation as a counterbalance to downside risks, illustrating that while headline pressures are moderating, underlying price pressures remain robust. Overall, the data suggest a balanced inflation outlook: the Eurozone continues to experience a stable environment near the ECB’s target, yet persistently high services inflation underscores the rationale for the ECB’s cautious and measured policy stance.

We expect inflation to remain near the ECB’s target and do not anticipate further rate cuts this year unless a significant, unexpected development occurs.