Back

Insights

EU Economy: Weekly Commentary – November 10, 2025

European Market Review

Adrian Van Den Bok and David Pintado

CEO

European Market Review

European bond yields rose, with Italy’s bonds lagging. Stocks fell, led by Portugal and France. Euro gained 0.26%. Brent crude dropped amid rising output and weaker Chinese demand.

European bond yields rose over the past week. The spread between German and French 10-year bonds widening to 79.3 basis points. Despite major investment firms and credit rating agencies signalling improving prospects for Italy, Italian bonds were the week’s worst performers. Olaf Sleijpen, Governor of the Dutch Central Bank and member of the ECB Governing Council, cautioned that the introduction of Eurobonds could lead to higher debt levels and urged consideration of alternative measures, such as reforming the EU budget framework, noting that “Europe can be built with or without Eurobonds.” European equity markets ended the week in negative territory, led by Portugal (−2.85%) and France (−2.10%). The euro appreciated 0.26% against the US dollar, while Brent crude fell 1.36% amid rising output from the US and OPEC+, fuelling concerns about potential oversupply. Saudi Arabia’s decision to cut December prices for Asian buyers, reflecting weaker demand, particularly from China, further weighed on market sentiment.

Week: 03 – 07 November | |||||

Stock Market | Last | % CHG | Currency | Last | % CHG |

Euro Stoxx | 5566.53 | -1.69 | EUR/USD | 1.1566 | 0.26 |

Stoxx Europe 600 | 564.79 | -1.24 | Commodities | Last ($) | % CHG |

France | 7950.18 | -2.10 | Brent | 63.70 | -1.36 |

Germany | 23569.96 | -1.62 | Bond Market - 10 Years | Last | BP |

Italy | 42917.67 | -0.60 | Germany | 2.672% | 3.76 |

Portugal | 8186.96 | -2.85 | France | 3.464% | 4.21 |

Spain | 15901.40 | -0.82 | Italy | 3.438% | 7.49 |

Belgium | 4914.46 | 0.25 | Spain | 3.190% | 4.07 |

Europe View Synopsis

The Eurozone grew fastest since May 2023, driven by services and Spain, while retail sales fell and German industry showed modest recovery amid weak manufacturing and cautious consumption.

The Eurozone economy experienced its fastest growth since May 2023 in October, led by the services sector and strong performance in Spain, supported by rising employment, robust domestic demand, and easing input cost inflation, while manufacturing remained subdued. The Composite PMI rose to 52.5, a 29-month high, with services activity at a 17-month peak, although France saw output decline. Employment growth accelerated to a 16-month high, and firms raised prices despite moderating cost pressures, maintaining cautious optimism. Meanwhile, Eurozone retail sales fell 0.1% month-on-month in both August and September, as households prioritized savings despite higher wages and improving confidence, reflecting persistent uncertainty and subdued consumption. In Germany, industrial production rebounded modestly by 1.3% in September after a sharp decline in August, with gains in automotive and electrical equipment sectors offset by weaker energy-intensive industries. Structural challenges, weak global demand, and high costs suggest a broad-based industrial recovery is unlikely before 2026. Overall, growth is supported by services and domestic demand, while manufacturing and consumption remain restrained.

Business Activity

The Eurozone economy grew at its fastest pace since May 2023 in October, led by services and Spain, with rising employment, strong domestic demand, modest export weakness, and easing input cost inflation.

The Eurozone economy recorded its strongest expansion since May 2023 in October, with the Composite PMI rising from 51.2 to 52.5, a 29-month high, while the Services PMI Business Activity Index climbed to 53.0, a 17-month peak. Growth was led by the services sector, where new business volumes increased at the fastest pace in two-and-a-half years, fully offsetting stagnant manufacturing orders. Spain posted the sharpest rise in private sector activity, followed by Germany, which saw business activity accelerate to its strongest level in almost two-and-a-half years. Ireland and Italy also registered solid expansions, whereas France remained an outlier, with output contracting at an eight-month low. Employment growth quickened to a 16-month high, driven by services, and overall workloads were effectively managed despite backlogs rising marginally for the first time in a year-and-a-half. Input cost inflation eased for a second consecutive month, yet companies raised selling prices at the fastest pace in seven months. Domestic demand underpinned growth, while new export orders continued to decline modestly. Firms remained cautiously optimistic about the year ahead, though confidence dipped slightly from September.

We expect the Eurozone economy to maintain moderate expansion, underpinned by services and domestic demand, while overall business activity remains subdued, primarily constrained by weak manufacturing performance.

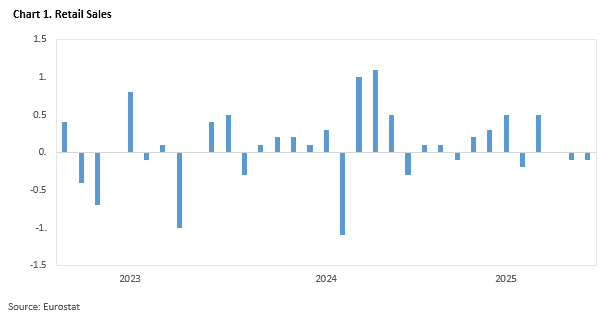

Retail Sales

Eurozone retail sales fell 0.1% MoM in August and September, as consumers, despite higher wages and confidence, prioritised savings amid lingering economic uncertainty and cautious spending.

Eurozone retail sales have once again slipped into decline, underscoring the persistent gap between improving household finances and consumer spending behaviour. Despite solid real wage growth and a gradual recovery in consumer confidence, retail sales fell by 0.1% MoM in both August and September, extending a weak trend that began after June, the last month to record any growth. In September 2025, the volume of retail trade across the euro area remained stable for food, drinks, and tobacco, but decreased by 0.2% MoM for non-food products (excluding automotive fuel) and by 1.0% MoM for automotive fuel sold in specialised stores. This continued weakness is surprising given that purchasing power has strengthened significantly since 2023, when wage growth started consistently outpacing inflation. However, households appear to remain cautious, directing additional income toward savings rather than consumption. Consumer confidence has improved from -16.6 to -14.2, yet it remains below its long-term average, reflecting ongoing uncertainty about the broader economic outlook. According to the European Commission, savings intentions reached an all-time high in October, suggesting that even with higher disposable incomes, consumers are prioritising financial security over spending. This restrained approach to consumption, despite favourable income conditions, poses a risk to overall demand and signals subdued consumption growth for the Eurozone in the third quarter.

We expect that Eurozone retail sales will remain subdued in the coming months, as consumers continue prioritising savings over spending despite higher wages, improved confidence, and stronger purchasing power.

German Industrial Production

German industry shows a modest rebound, with production up 1.3% MoM. Structural weaknesses, weak global demand, and high costs mean a sustained recovery remains unlikely before 2026.

German industry is showing tentative signs of recovery, with industrial production rising by 1.3% MoM in September after a sharp 3.7% decline in August, while factory orders increased for the first time in five months, up 1.1% overall and 1.9% excluding large, volatile one-off orders, driven mainly by the automotive and electrical equipment sectors. Nevertheless, the rebound remains too modest to indicate a structural turnaround, as industrial production is still down 1% YoY and energy-intensive sectors such as chemicals, metals, and paper continue to operate below pre-crisis levels. The September improvement largely reflects a correction following the weak August data, which was distorted by temporary factors including summer holidays and production adjustments in the automotive industry. Although activity in the automotive and electronics sectors provided the main boost, overall manufacturing output declined and construction activity fell by 0.9% MoM after three consecutive months of gains. Despite some encouraging signs such as improving production expectations, healthier order books, lower inventories, and stronger public demand for defence and infrastructure projects, German industry continues to face persistent cyclical and structural challenges. Weak global trade, subdued Chinese demand, elevated energy prices, tight financing conditions, and low capacity utilisation continue to weigh on confidence and investment. While a more expansionary fiscal stance expected next year may offer some support, a sustained and broad-based recovery in German manufacturing remains unlikely before the second half of 2026.

We don’t expect any significant improvement in the short term. German industry shows only a modest rebound, with production up 1.3% MoM, while structural weaknesses, weak global demand, and high costs continue to weigh on growth.