Back

Insights

US Economy: Weekly Commentary – October 27, 2025

US Market Review

Adrian Van Den Bok and David Pintado

CEO

US Market Review

U.S. yields diverged, with short-term rates falling. Equities advanced broadly. The euro weakened slightly. Oil surged on Russian sanctions, while gold declined and Bitcoin rose modestly.

U.S. Treasury yields declined at the short end of the curve, while medium- and long-term yields edged slightly higher. The yield on the 10-year Treasury fell below 4%, as mounting credit concerns weighed on regional bank stocks. The move followed remarks from JPMorgan CEO Jamie Dimon, who warned of potential credit “cockroaches.” The decline in yields also underscores the market’s growing conviction that the Federal Reserve will move to lower interest rates.

U.S. equities advanced broadly over the week. Micro- and small-cap stocks gained 3.40% and 2.50%, respectively, while large-cap equities rose 1.90%. The “Magnificent 7” climbed 2.40%. Sector performance was led by technology (+3.0%) and energy (+2.4%), while utilities (-0.2%) and consumer staples (-0.8%) posted modest declines. Market volatility eased notably, with the VIX falling more than 20%.

The U.S. dollar appreciated 0.22% against the euro. WTI crude oil surged 6.59% following new U.S. sanctions on Russia’s largest oil producers, Rosneft and Lukoil, which are expected to tighten global supply. The measures freeze assets, prohibit U.S. transactions, and impose potential penalties on foreign firms purchasing Russian oil, prompting refiners in China and India to scale back imports. Meanwhile, gold declined 3.31% over the week, while Bitcoin gained 0.70%.

Week: 20 - 24 October | |||||

Stock Market | Last | % CHG | Commodities | Last | % CHG |

S&P 500 | 6791.69 | 1.92 | WTI | 61.44 | 6.59 |

Nasdaq 100 | 25358.16 | 2.18 | Gold | 4126.60 | -3.31 |

Russell 2000 | 2513.47 | 2.50 | Currency | Last | % CHG |

Bonds | Last | BP | USD/EUR | 0.8597 | 0.22 |

US - 10 Years | 4.023% | 0.90 | Cryptocurrency | Last | % CHG |

US - 2 Years | 3.501% | 2.90 | Bitcoin | 111030.10 | 0.7 |

US Market Views Synopsis

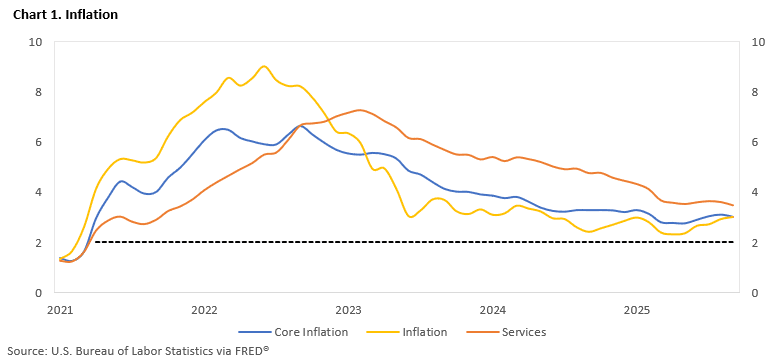

US growth remains moderate, led by services and domestic demand. Inflation eased, with headline and core CPI at 3.0% YoY. Employment grew modestly, exports fell, and business confidence weakened.

US economic data for October show a resilient economy alongside easing inflation. Headline CPI rose 3.0% YoY in September, with core services moderating to 3.5% and core goods steady at 1.5%. Housing inflation remained subdued, while energy costs increased due to gasoline. Tariff effects on consumer prices were limited, as companies shifted sourcing to lower-cost suppliers. Disinflationary forces, including moderating rents, easing energy costs, and a cooling labour market, support expectations for a 25bp Fed rate cut. Business activity accelerated in October, with the Composite PMI at 54.8, driven by strong services growth (55.2) and modest manufacturing expansion (52.2). New orders rose sharply, though exports fell amid tariffs, while backlogs fell and finished goods inventories surged. Employment growth was modest, concentrated in services, and input costs remained elevated, though output prices rose at the slowest rate since April. Consumer sentiment declined slightly, with younger gains offset by older losses, and year-ahead inflation expectations eased to 4.6% YoY while long-term expectations rose to 3.9% YoY. Overall, US growth is expected to continue moderately, supported by domestic demand and services.

Inflation

US September inflation softened, with headline 3.0% YoY, core services easing to 3.5%, limited tariff impact, cooling labour market, supporting 25bp Fed rate cut.

US inflation in September was softer than anticipated, with headline CPI rising 0.3% MoM (3.0% YoY) and core CPI, excluding food and energy, increasing 0.2% MoM (3.0% YoY), below consensus expectations of 0.4% and 0.3% MoM, respectively. In year-over-year terms, core services moderated to 3.5%, while core goods remained steady at 1.5%. Core goods advanced modestly by 0.2% MoM, with apparel up 0.7% and new car prices rising 0.2%, offset by declines in used cars (-0.4%) and medical care commodities (-0.1%). Housing inflation remained subdued, with owners’ equivalent rent up 0.1% and primary rents rising 0.2%. Energy costs increased 1.5%, driven primarily by a 4.1% rise in gasoline, and additional upward pressures were observed in airline fares (+2.7% MoM) and tobacco (+0.6%), although broader declines in global energy prices are expected to temper these components in the coming months. Tariff effects remain limited, with realised rates around 10%, well below the 18% projected based on announced tariffs, as companies shift sourcing to lower-cost suppliers, mitigating pass-through to consumer prices; any tariff-driven inflation is expected to be transitory rather than persistent. Disinflationary forces are building elsewhere, supported by falling housing prices, moderating rents, easing energy costs, and a weakening labour market, which is reducing wage pressures. Collectively, these developments support a 25 basis-point Federal Reserve rate cut next week and reinforce expectations for a cumulative 100 basis points of easing, even as the cooling labour market becomes the Fed’s more pressing concern for achieving its dual mandate of price stability and maximum employment.

We continue to anticipate a 25 basis-point rate cut next week, supported by easing inflation and a weakening labour market.

Business Activity

US growth accelerated in October, led by services and domestic demand. Manufacturing expanded modestly, exports fell, inventories surged, employment grew modestly, input costs remained high, and business confidence weakened.

The US economy began the fourth quarter strongly, with the Composite PMI rising to 54.8 in October from 53.9 in September, marking the second-fastest expansion so far this year. Services led growth, with the Business Activity Index climbing to 55.2, reflecting robust domestic demand and the steepest rise in new orders in 2025, while manufacturing output also strengthened, with the Manufacturing PMI at 52.2. Despite higher production, exports fell sharply in both sectors, driven by tariffs and weaker overseas demand, while factories faced falling backlogs of work but unprecedented accumulation of finished goods stock, indicating excess capacity and challenges in selling produced goods. Input costs remained elevated due to tariffs and rising wages, yet overall output prices increased at the slowest rate since April as firms competed for domestic sales. Employment growth picked up modestly, concentrated in services, while manufacturing hiring slowed, constrained by limited candidate availability and cautious staffing decisions. Business confidence fell to one of the lowest levels in three years, reflecting concerns over government policies, trade uncertainty, and the impact of tariffs, though lower interest rates provided some support. Overall, the data indicate sustained US economic growth at the start of Q4, driven by strong service sector momentum, resilient domestic demand, continued manufacturing expansion, and ongoing challenges in managing inventories and export performance.

We anticipate that US economic growth will sustain a moderate and steady pace. The expansion is underpinned by resilient domestic demand and robust services activity. Ongoing tariff pressures, export weakness, and elevated input costs may constrain momentum.

Consumer Sentiment

Consumer sentiment edged down 1.5 points. Gains among younger consumers were offset by declines in older groups. Inflation concerns persist, long-term expectations rose, and government shutdown impact remained minimal.

Consumer sentiment remained largely unchanged this month, declining marginally by 1.5 index points from September. Gains in sentiment among younger consumers were offset by declines among middle-aged and older groups. While current personal finances showed a slight improvement, expectations for future finances weakened. Overall, consumers perceive minimal changes in economic conditions compared with last month, with inflation and high prices continuing to dominate concerns. The federal government shutdown had little apparent impact on perceptions, with only 2% of respondents spontaneously mentioning it, compared with 10% during the 35-day shutdown in January 2019. Year-ahead inflation expectations eased slightly to 4.6% from 4.7% last month, situating them between the levels seen a year ago and the peaks recorded in May following initial tariff announcements. Long-term inflation expectations rose to 3.9% from 3.7% last month, primarily driven by independents and Republicans, though remaining below this year’s April high. Inflation uncertainty, as measured by the interquartile range of expectations, increased modestly for both time horizons.

We expect consumer sentiment to remain steady short-term. Inflation concerns may persist, while the impact of government shutdowns is likely to stay minimal.